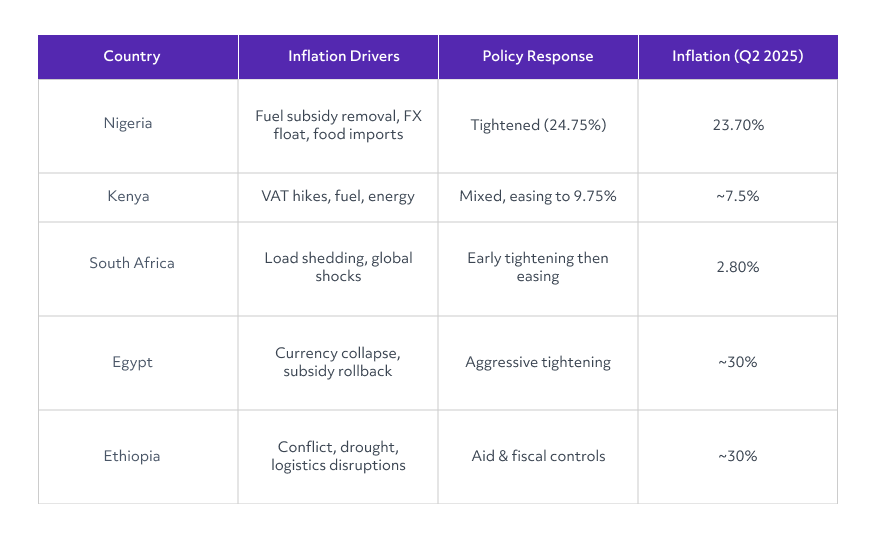

Inflation is shaping Africa’s future in complex and uneven ways. Between 2022 and 2025, countries like Nigeria and Egypt saw historic spikes driven by subsidy cuts and currency reforms, while South Africa and Kenya managed more measured paths through early policy tightening.

Nigeria stands out for both the severity of its inflation and the depth of its human impact. Following the removal of fuel subsidies and the floatation of the naira in 2023, inflation rose sharply, peaking at 34.8% in December 2024 (NBS). Though it moderated to 23.7% by April 2025, cost-of-living pressures remain extreme.

Insights from Versus’ Nigeria Scout survey reveal how inflation affects everyday decisions: eating fewer meals, walking instead of commuting, borrowing to buy food, or juggling informal side hustles. Over half of Nigerians surveyed had taken credit in the past year, often for basic survival needs.

This report brings together:

The findings aim to inform policymakers, fintech innovators, funders, and civil society organizations who are navigating the long shadow of inflation across Africa.

Inflation is no longer just a macroeconomic issue in Africa, it’s a daily struggle that defines how people eat, work, commute, and survive. In the wake of multiple global and local shocks, from the war in Ukraine to fuel subsidy reforms and currency devaluations, African economies have seen cost-of-living crises ripple through every layer of society.

This report, produced by Versus Africa, takes a pan-African view of inflation’s drivers, sectoral impacts, and policy responses, while using Nigeria as the focal point for on-the-ground insight through new primary data from our Scout research network.

We explore how inflation is being felt in real time, what trade-offs households are making, which financial tools people turn to in moments of hardship, and what innovations are emerging to help. Our approach combines macroeconomic analysis, survey data, and grounded narratives to paint a full picture of inflation’s pulse across the continent.

The report focuses on five key countries: Nigeria, Kenya, Egypt, Ethiopia, and South Africa, chosen for their regional and economic significance, diversity of policy responses, and accessibility of data. These countries illustrate both the shared and divergent paths African nations are taking in the face of inflation.

Africa’s inflation story is shaped by both global disruptions and country-specific policy choices. Food prices remain the biggest driver continent-wide, followed by transport and housing. Currency pressures, fuel dependency, and fiscal reform have amplified inflation in some contexts more than others.

Data Sources: CBN.gov.ng, KNBS.or.ke, CentralBank.go.ke, ParthianPartnersNG.com, CytonnReport.com, MPRA.ub.uni-muenchen.de, NESgroup.org, SARB (South African Reserve Bank), IMF World Economic Outlook (Apr 2024), World Bank Global Economic Prospects, CAPMAS (Egypt), Ethiopia Central Statistics Service. Data visualization by Versus Africa

.png)

Data Sources: Trading Economics, IMF World Economic Outlook (Apr 2024), World Bank Global Economic Prospects, AfDB Economic Outlook. Data visualization by Versus Africa

Insights: From 2019 to 2025, inflation in Nigeria and Egypt spikes sharply after 2022, driven by FX reforms and subsidy removal. Ethiopia remains persistently high due to conflict and food shortages. Kenya peaks around 2023 and begins to stabilize. South Africa stays relatively stable throughout the period.

Key Takeaway: Countries with stronger monetary frameworks (like South Africa) show better inflation control. Meanwhile, subsidy removal, exchange rate instability, and debt exposure drive inflation spikes in Nigeria and Egypt.

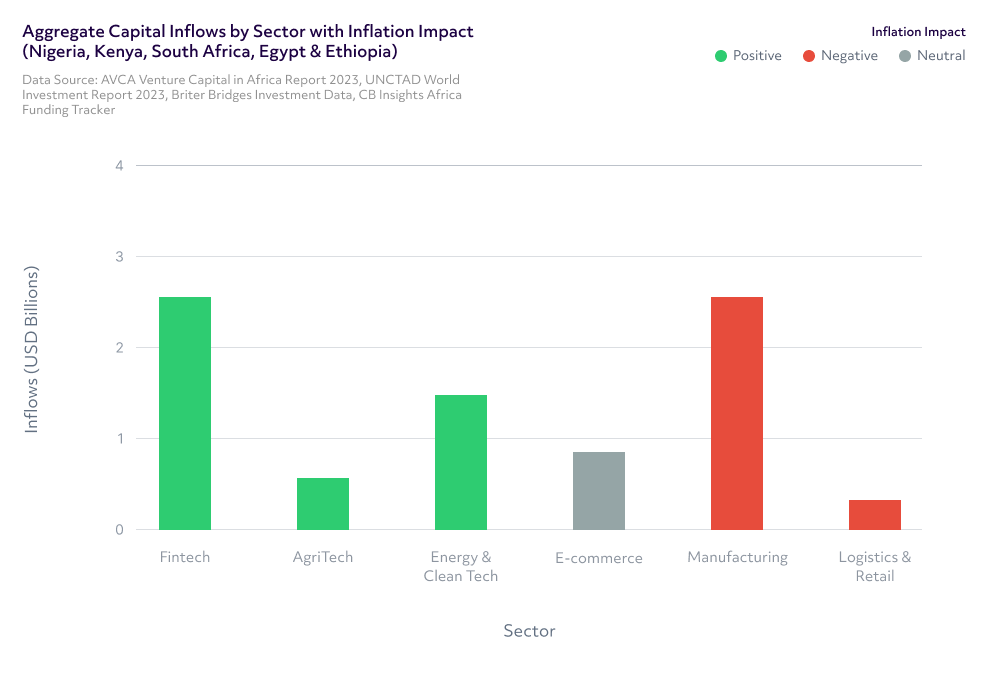

While fintech, telecoms, and logistics show resilience due to investor support, sectors like agriculture, food processing, healthcare, and local manufacturing remain highly inflation-sensitive and underinvested. These are the sectors where costs rise fastest and access drops for vulnerable populations.

Data Sources :AVCA Venture Capital in Africa Report 2023, UNCTAD World Investment Report 2023, Briter Bridges Investment Data, CB Insights Africa Funding Tracker. Data visualization by Versus Africa.

Insights: Across Nigeria, Kenya, South Africa, Egypt, and Ethiopia, capital inflows were highest in fintech, manufacturing (especially extractives), and energy/clean tech with notable investments also going into agritech and e-commerce. While fintech, agritech, and clean energy sectors helped consumers by expanding access to credit, food systems, and alternative energy, e-commerce had a mixed impact, offering convenience and supply chain efficiency, but also exposing consumers to higher costs due to FX-linked imports. In contrast, sectors like logistics, and parts of manufacturing felt intensified inflationary pressure due to foreign exchange volatility and rising import costs.

Data Sources: AVCA Venture Capital in Africa Report 2023, UNCTAD World Investment Report 2023, Briter Bridges Investment Data, CB Insights Africa Funding Tracker. Data visualization by Versus Africa.

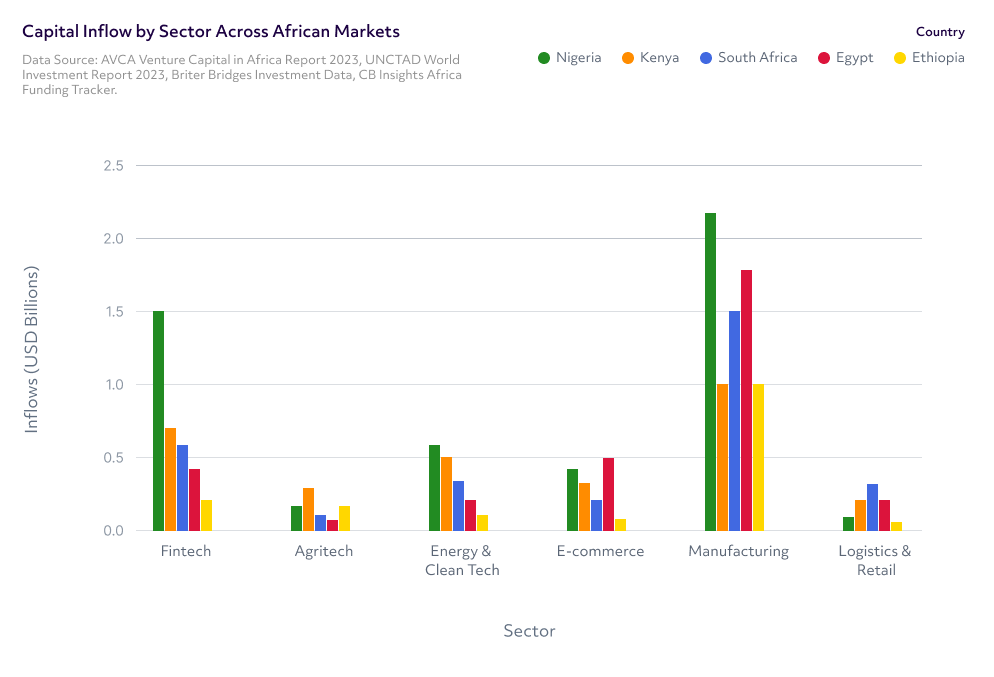

Capital Inflow Impact to Inflation Per Industry Across Five African Economies

Data Sources: AVCA Venture Capital in Africa Report 2023, UNCTAD World Investment Report 2023, Briter Bridges Investment Data, CB Insights Africa Funding Tracker. Data visualization by Versus Africa.

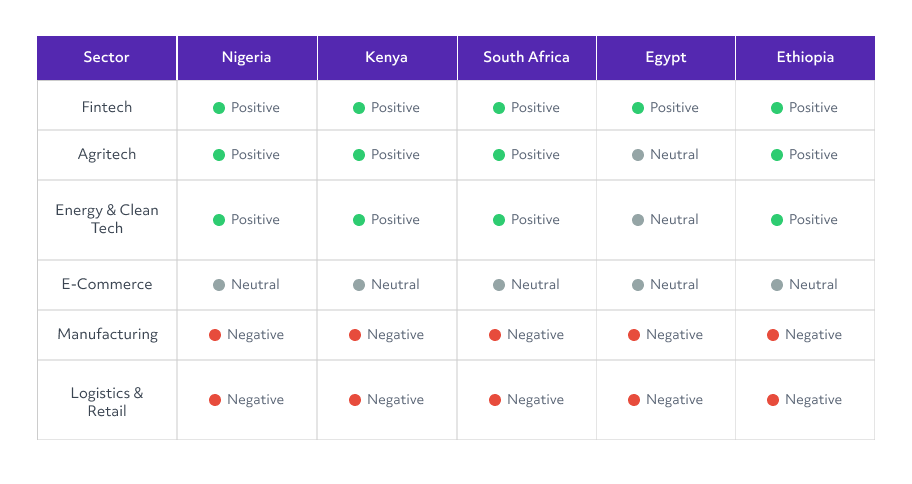

The table above shows the inflation impact of capital inflows across six key sectors in five African countries — Nigeria, Kenya, South Africa, Egypt, and Ethiopia. Each cell reflects whether the sector’s growth helped cushion inflation (🟢 Positive), had minimal or mixed impact (⚫ Neutral), or worsened inflation pressures (🔴 Negative).

This table helps summarize how sector-level capital inflows interacted with inflation dynamics in each country, highlighting which investments supported consumer resilience and which sectors amplified economic strain.

Insights: Across countries, these patterns were consistent: fintech, agritech, and clean tech generally had a positive inflation impact, especially in Nigeria and Kenya. Manufacturing and logistics, particularly in Egypt and Ethiopia, tended to have a negative impact, while sectors like e‑commerce showed a neutral effect across most markets.

Key Takeaway: Capital inflows drove innovation and consumer relief in resilient sectors such as fintech and clean energy, particularly in Nigeria and Kenya.

However, FX-dependent and import-heavy sectors like logistics and manufacturing, faced worsening inflationary effects, showing that capital alone cannot offset weak policy or macro shocks.

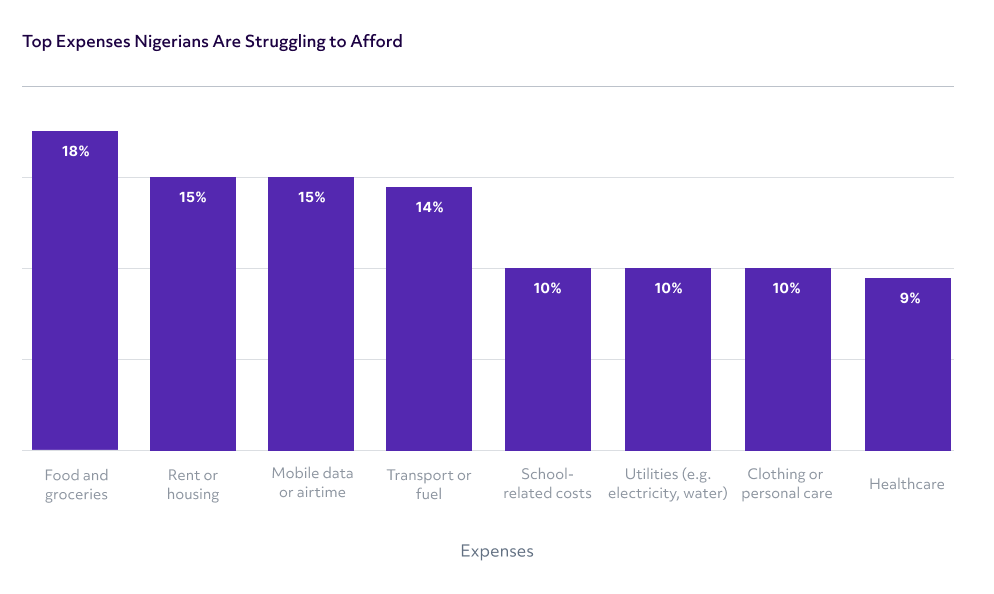

Result from Versus Ask. 300+ respondents across Nigeria

Question: Which expenses have become hardest to afford recently?

Insights: Food and groceries top the list, with nearly 1 in 5 respondents citing them as their hardest expense. Transport, mobile data, and rent follow closely, showing that daily essentials and digital access are now serious affordability concerns. The fact that education, healthcare, and utilities rank high underscores the depth of inflation’s impact across core survival and social mobility needs.

Nigerians are navigating one of the most painful inflation episodes in the country’s democratic history. Following fuel subsidy removal and naira float, the cost of transport, food, and household items surged. A bag of rice doubled in price. Garri, cooking oil, and bread became luxuries for many families.

“The cost of food, transportation, and other basic needs is now on the high side. I now do more trekking.” — Male, Lagos, 36–45

“It has deprived me of so many privileges in terms of transportation and feeding.” — Female, Abuja, 26–35.

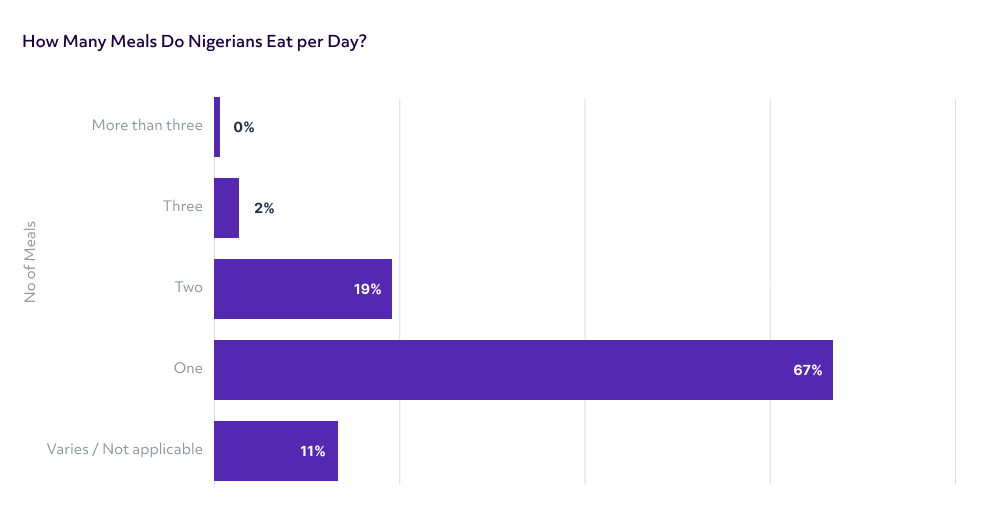

Result from Versus Ask. 300+ respondents across Nigeria

Question: How many meals do you or your household now eat per day (on average)?

Insights: A staggering 67% of Nigerian households now eat only one meal per day, reflecting severe food insecurity driven by rising inflation. Just 2% maintain a three-meal routine, and 11% report variability, likely due to inconsistent income or food access. This is not just a dietary shift, it’s a survival strategy under economic duress.

Small business owners are some of the hardest hit. Transporters, food vendors, and market traders report lower demand and shrinking margins.

“It has affected me a lot because I lost my job due to inflation.” — Male, Delta, 18–25

“Because of inflation I now work more hours, but earn far less.” — Female, Lagos, 26–35

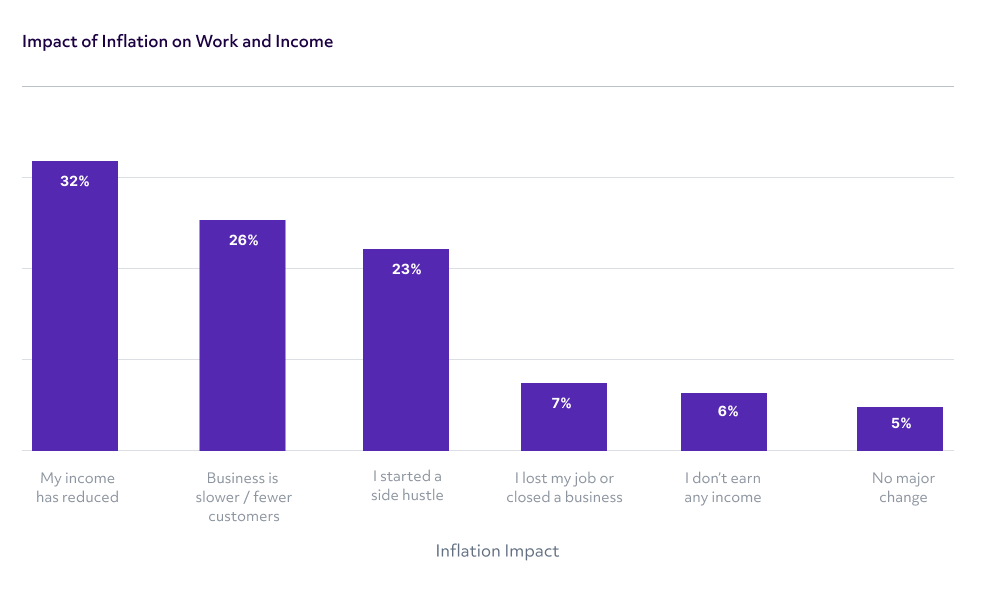

Result from Versus Ask. 300+ respondents across Nigeria

Question: How has inflation affected your income or work?

Insights: A majority of respondents report significant economic disruption due to inflation: 32% say their income has dropped, while 26% cite reduced business activity. In response, 23% have started side hustles, highlighting a pivot to informal or entrepreneurial solutions as coping mechanisms.

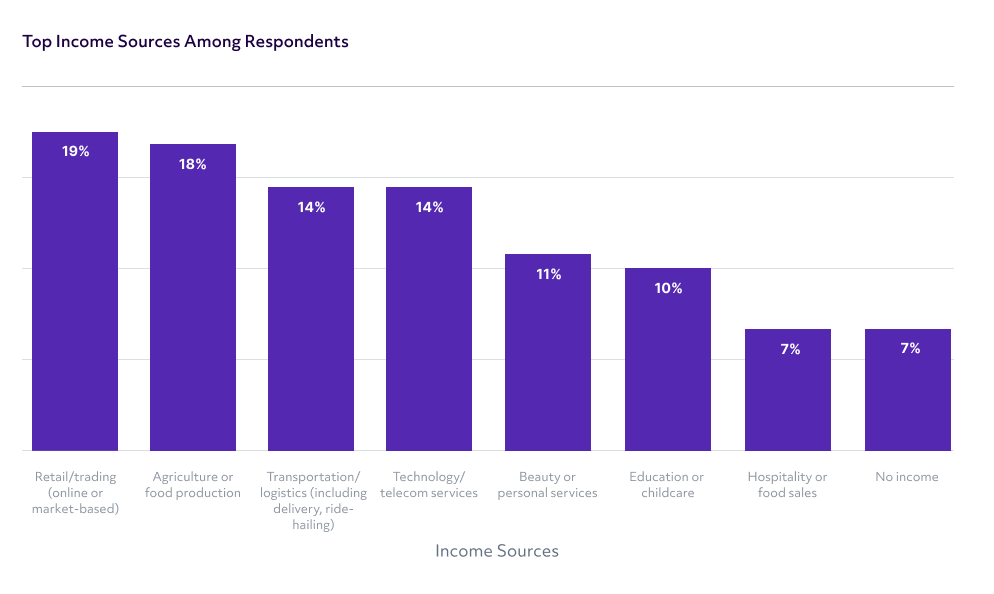

Result from Versus Ask. 300+ respondents across Nigeria

Question: Which of the following sectors are you currently earning income from?

Insights: The income landscape reveals a deeply informal and entrepreneurial economy. Retail trading (19%) and agriculture (18%) lead as the most common income sources, followed closely by transportation and logistics (14%). Notably, digital-era sectors like beauty services and technology trail behind, showing that despite digital tools gaining popularity, everyday earnings still come from traditional, hustle-based sectors.

Many are shifting to mobile commerce or informal barter arrangements. Women in particular, who dominate market-side retail, report skipping meals or rotating school fees and food purchases by week.

“The high cost of living has really made me budget for everything. We can't buy as we used to.” — Female, Ogun, 26–35

“Cutting down on feeding and other things to survive.” — Male, Rivers, 36–45

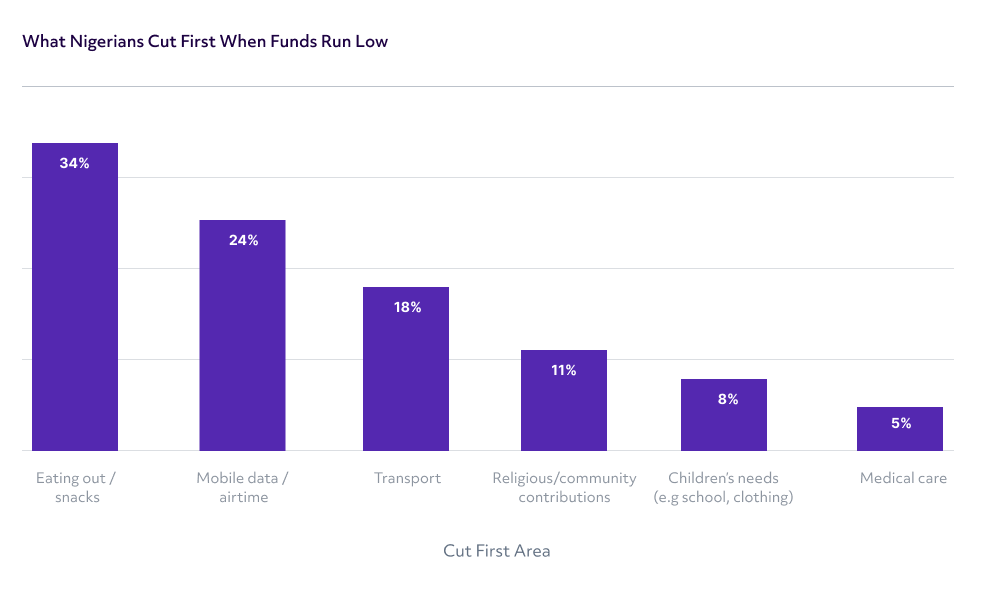

Result from Versus Ask. 300+ respondents across Nigeria

Question: What do you reduce or cut first when money is tight?

Insights: When faced with financial strain, Nigerians prioritize cutting non-essential or flexible expenses first. Eating out/snacks (34%) and mobile data/airtime (24%) are the most commonly sacrificed, while transport (18%) follows closely. Interestingly, even religious or community contributions (11%) and children’s needs (8%) are on the chopping block for some households. The fact that 5% report cutting back on medical care is a worrying indicator of how survival trade-offs can endanger well-being.

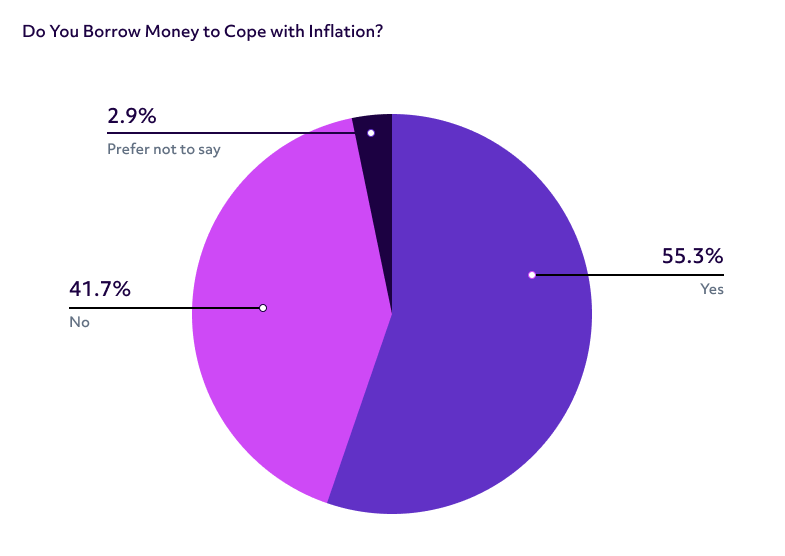

Result from Versus Ask. 300+ respondents across Nigeria

Question: Have you used any kind of loan or credit in the past 12 months?

Insights: More than half (55%) of respondents reported taking some form of credit or loan in the past year, highlighting the increasing reliance on borrowing as a coping mechanism during inflation. While 42% said no, and 3% preferred not to answer, the high “yes” response underscores the growing role of credit in day-to-day survival, not just for investment, but often to cover basic needs.

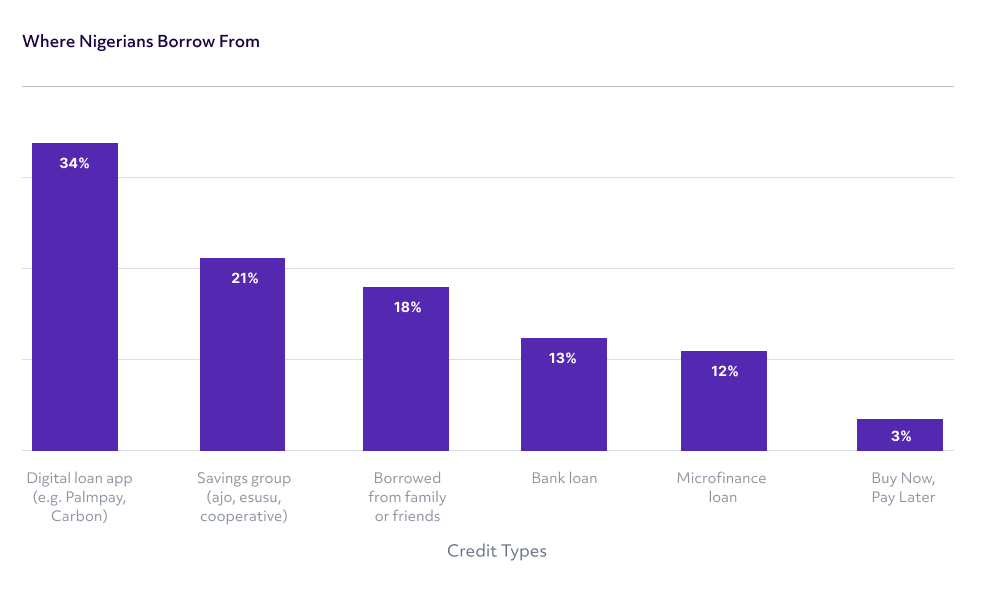

Result from Versus Ask. 300+ respondents across Nigeria

Question: What types of credit have you used?

Insights: Digital loan apps lead as the top source of borrowing (34%), narrowly ahead of traditional savings groups like ajo and cooperatives (21%). While formal bank and microfinance loans remain in use, their reach is limited compared to informal and digital options, highlighting trust, access, and speed as major decision drivers.

Digital lending platforms like PalmPay, FairMoney, and Carbon have become increasingly popular, especially among young urban residents. However, the relief is temporary, most loans have repayment periods under 30 days, often with interest rates exceeding 30% APR, leading to rolling debt traps.

“I now rely on borrowing small amounts from different people to keep up.” — Female, Kaduna, 26–35

“Things are so expensive I sometimes use loan apps to buy food or pay bills.” — Male, Lagos, 26–35

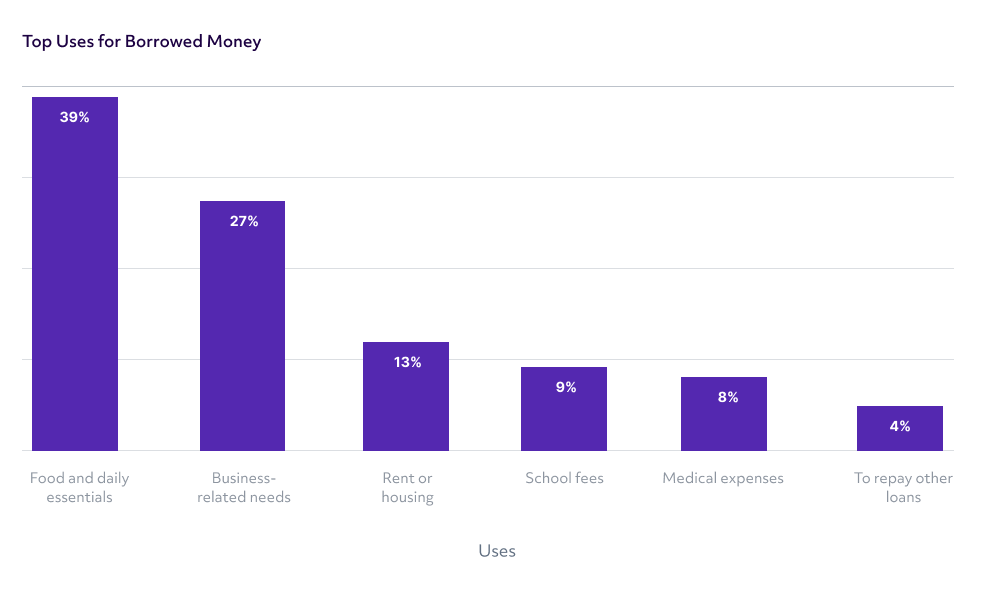

Result from Versus Ask. 300+ respondents across Nigeria

Question: What did you use the loan or credit for?

Insights: Over a third of respondents (39%) reported borrowing to afford food and daily essentials, with business support and rent following closely. Education and medical needs also appear, but less prominently. Notably, 4% are already caught in debt cycles, borrowing to repay existing loans, highlighting growing financial fragility.

Result from Versus Ask. 309 respondents across Nigeria

Question: How do you feel about using digital loans or credit apps?

Insights: Nigerians are split in their views on digital loans. While 44% acknowledge they are helpful or necessary despite high interest, a larger share, 39%, express negative sentiment, describing them as stressful or untrustworthy. This highlights a growing reliance on short-term credit for survival, but also rising concerns over repayment pressure and trust in the system. Notably, 18% have never used digital credit, indicating limited reach among some demographics.

Households are adapting in real time:

“We have had to cut costs for some things we normally get in the family.” — Female, Oyo, 36–45

“The issue is that I have to reduce everything that I used to do to have a good living.” — Male, Plateau, 26–35

Result from Versus Ask. 300+ respondents across Nigeria

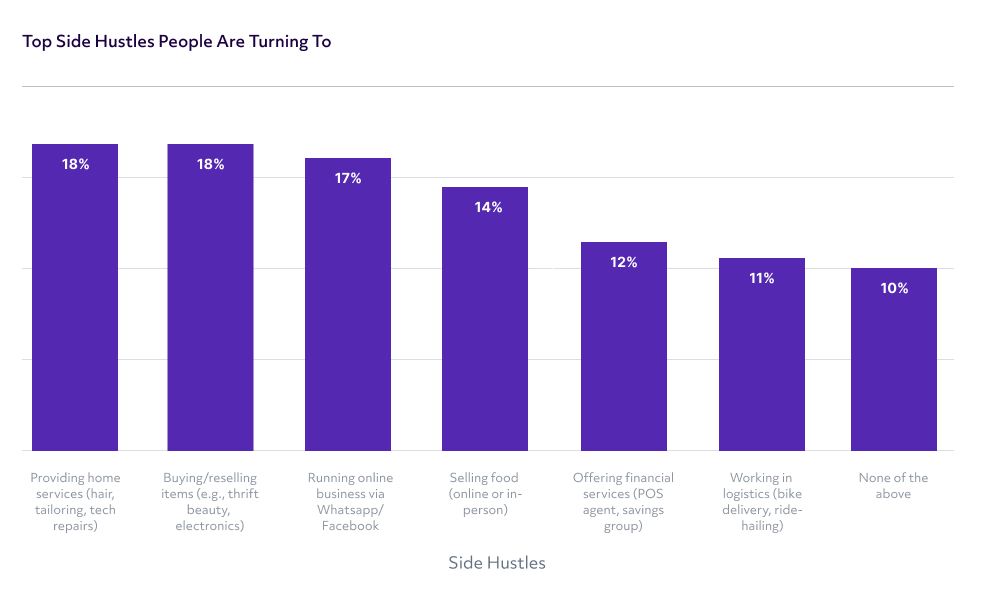

Question: Are you or someone in your household doing any of the following to survive rising costs?

Insights: In the face of skyrocketing prices, Nigerians are hustling harder than ever to stay afloat. The most common income-generating tactics include home services, item reselling, online businesses, and food sales, underscoring a shift toward informal, survival-based entrepreneurship.

In Kenya, inflation has softened thanks to early monetary tightening, but for the average consumer, life remains expensive, particularly when it comes to transport and staple food items.

Egypt's inflation crisis is fueled by a steep devaluation of the Egyptian pound and reduced subsidies as part of IMF-backed reforms. The result has been widespread public dissatisfaction, especially among middle-class households now dependent on government assistance.

Still reeling from internal conflict and drought, Ethiopia faces a more localized but equally severe inflation crisis, particularly around food.

South Africa’s inflation rate has been relatively stable, thanks to strong institutions and early policy moves. Yet even modest inflation is proving burdensome for working-class households.

Data Sources: Afrobarometer Report PDF (May 2024); Reuters – “S. Africa consumer confidence recovers in Q2, survey shows” (June 27, 2024). Data visualization by Versus Africa.

Insights: Sentiment data (on a scale of 0 to 10, where 10 indicates extreme price pressure) shows Egypt scoring 9.2, the highest among the five countries, due to sharp currency devaluation and subsidy cuts that have triggered widespread price shocks and reliance on state rations. Nigeria follows closely at 8.7, reflecting the public’s reaction to fuel subsidy removal and FX reforms, which significantly raised transport and food costs. Ethiopia scores 7.9, driven by persistent conflict and food insecurity that continue to strain household expenses. In Kenya, the perception index stands at 7.5, as rising fuel costs and new taxes increase pressure despite coping mechanisms like mobile credit and savings groups. South Africa records the lowest score of 5.6, where strong monetary controls have kept consumer inflation relatively manageable despite global economic pressures.

Key Takeaway: Perception mirrors economic pain , countries undergoing aggressive reforms (like Egypt and Nigeria) feel the most pressure, while South Africa’s relative stability reflects well in consumer sentiment.

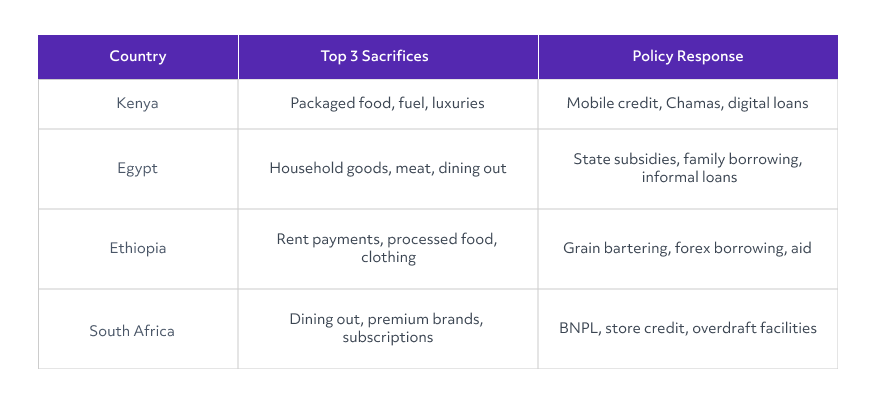

Top Spending Sacrifices and Credit Reliance Across 4 African Countries

Data Sources: Business Daily – “Consumers turn to loose grains as inflation bites” , Reuters – “Egypt’s headline inflation jumps to 16.8% in May” , Reuters – “Ethiopia's inflation squeezes family budgets as food prices rise” (Mar 2023) , News24 – “Things are becoming more expensive: Shoppers struggle to keep up with rising cost of living” . Data visualization by Versus Africa.

Insights: Across the four countries, consumers are scaling back on non-essential and high-cost items to survive inflation. In Kenya and South Africa, packaged food, fuel, and lifestyle expenses are commonly sacrificed, while Egypt and Ethiopia show deeper cuts into basic goods like meat, rent, and clothing.

Credit tools vary by local infrastructure: Kenya leans heavily on mobile credit and Chamas, Egypt and Ethiopia depend more on informal borrowing and state support, while South Africa sees a rise in BNPL and formal credit facilities.

Key Takeaway: Consumers across Africa are adjusting spending in response to inflation, but their credit tools reflect local economic infrastructure with digital innovation filling formal banking gaps in Kenya, while traditional support systems dominate in Egypt and Ethiopia

Inflation is testing the resilience of traditional economic systems across Africa, but it has also triggered a wave of innovation, particularly in fintech, agriculture, and informal finance. These solutions vary widely by country and industry, reflecting both local needs and digital readiness.

Nigeria’s fintech ecosystem has been a leader in digital credit. Startups like Carbon, Branch, FairMoney, and PalmPay are extending micro-loans to underserved consumers using phone data and AI-based risk scoring.

Pros: Fast disbursement, low access barriers, mobile-friendly

Cons: Short repayment windows, rising defaults, interest rates >30% APR

“You can borrow ₦10,000 in five minutes, but you’ll owe ₦13,000 by month-end.” – Lagos tech market vendor

Platforms like PricePally enable group bulk-buying directly from farms or wholesalers. This has reduced food costs by up to 15–20% in some Lagos neighborhoods, especially for staple goods like rice and oil.

Digital Ajos (rotating savings groups) and co-ops now operate on WhatsApp, enabling real-time pooling of funds for food purchases, school fees, and rent. They often serve women and informal traders locked out of banking systems.

Twiga Foods connects smallholder farmers to urban vendors, streamlining distribution and reducing food inflation pressure. By removing middlemen, prices for tomatoes, onions, and maize have dropped by 10–18% in select regions.

Traditional savings groups (Chamas) have gone digital. Tools like Chamasoft and Pezesha help track contributions, automate lending, and access mobile credit.

“We now invest, save, and lend via an app, we don’t even meet in person anymore.” – Nairobi chama chair

Startups like Ecobodaa and Ampersand are accelerating electric motorcycle adoption, offering battery swap systems to cushion riders from rising fuel prices.

Large supermarkets like Pick n Pay and Checkers have introduced “Price Lock” bundles, 30-day guaranteed low prices on essentials. It’s a tactic to win loyalty amid price fatigue.

With over 70 million dependent on state rations, Egypt’s Ministry of Supply has digitized the ration card system, integrating biometric verification and SMS alerts to manage inflation shocks.

“Without the rice text alert, I wouldn’t even know what day to queue.” – Cairo mother of four

Apps like Wasfa and YallaCompare let users report and compare local prices of staples in real time. These tools have empowered shoppers but also revealed huge disparities.

In response to post-conflict shortages, informal food co-ops and community ration groups have emerged in cities like Addis Ababa and Bahir Dar. Many now operate via Telegram groups, pooling donations and food parcels.

Due to birr instability, some landlords and vendors now accept rent and food purchases in grain or USD equivalents, showing the emergence of barter-style inflation workarounds.

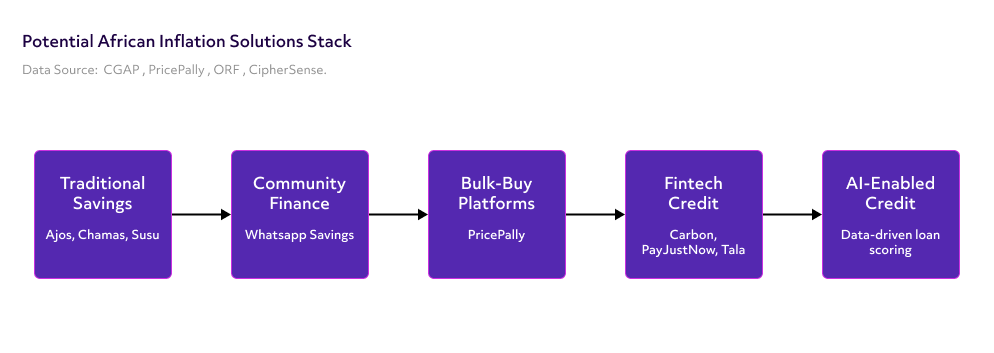

Data Sources: CGAP , PricePally , ORF , CipherSense. Data visualization by Versus Africa.

Key Insights: In response to rising living costs, Africans are relying on a mix of traditional and digital tools. At the base are community-driven savings systems like Ajos, Susus, and Chamas, which remain popular for their trust and accessibility. These are now increasingly digitized via WhatsApp and Telegram.

Above that, mobile fintech apps like Branch, Tala, and Carbon offer microloans and credit scoring using phone data, though defaults are rising due to poor regulation. Bulk-buy platforms like PricePally and Twiga reduce food costs by connecting buyers directly with producers. At the top of the stack, AI-powered credit scoring is emerging, but transparency and bias remain concerns.

Key Takeaway: From grassroots savings groups to AI-enabled lending, inflation solutions in Africa are evolving fast, but while digital innovation is expanding access, weak regulation and limited consumer education threaten long-term financial resilience.

Innovation is proving essential, but access remains unequal. Rural areas, older populations, and low-literacy consumers are often excluded from tech-based options.

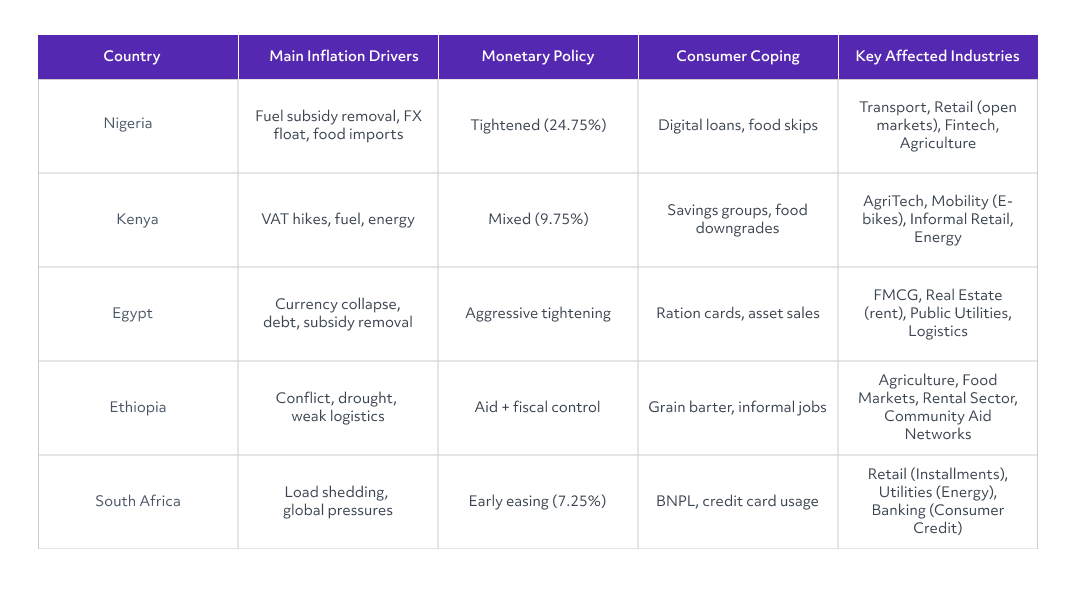

While inflation is a continental issue, its causes, impacts, and coping responses are highly contextual. Below is a comparative table showing not just economic policies and consumer behavior, but also the industries most affected or activated in each country.

Data Sources: Reuters – “Egypt’s headline inflation jumps to 16.8% in May”; Reuters – “Ethiopia's inflation squeezes family budgets as food prices rise” (Mar 2023); News24 – “Things are becoming more expensive: Shoppers struggle to keep up with rising cost of living”). Data visualization by Versus Africa

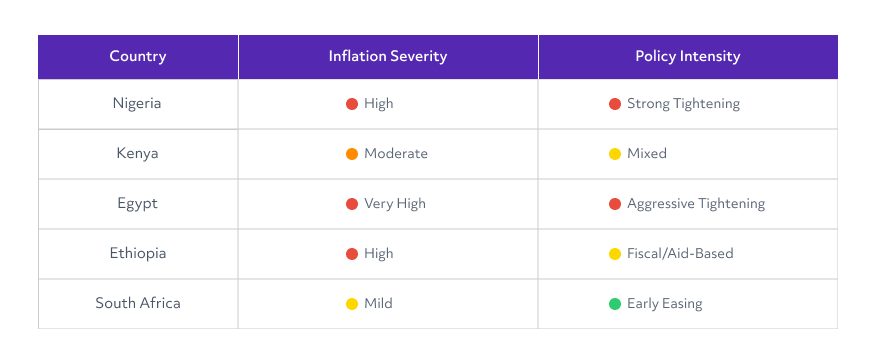

Inflation Severity vs Monetary Policy Response Across 5 African Countries

Data Sources: IMF World Economic Outlook, Trading Economics – Inflation Rate by Country, AfDB African Economic Outlook 2024. Data visualization by Versus Africa.

Key Insights: Each country is battling inflation from different angles. Nigeria and Egypt face the most severe inflation, largely due to currency reforms, subsidy cuts, and external debt pressures. Both have responded with aggressive monetary tightening, but consumers are coping through digital credit (Nigeria) or rationing and asset sales (Egypt), and key sectors like retail, utilities, and fintech are heavily affected.

Kenya and Ethiopia face moderate to high inflation, but policy responses are more mixed or fiscally driven. Citizens rely on informal systems like savings groups and bartering, with sectors like agritech, energy, and food markets adapting.

South Africa, by contrast, has milder inflation, thanks to early monetary easing and stronger policy institutions. Consumers are turning to BNPL and other formal credit tools, and the impact is more controlled across retail and energy sectors.

Key Takeaway: Africa’s inflation is widespread but uneven. Countries like Nigeria and Egypt are in crisis-mode, with severe consumer strain and aggressive policy reactions, while South Africa’s stronger monetary discipline offers relative protection. Coping strategies reflect both economic structure and innovation gaps, ranging from barter systems to mobile fintech.

This comparative lens highlights that inflation is not a one-size-fits-all crisis. Kenya’s relative stability contrasts with Egypt’s subsidy struggle, or Nigeria’s reform shock. The effectiveness of policy depends on public trust, institutional capability, and fiscal space.

Inflation in Africa is both imported and homegrown, policy matters as much as global shocks. While global disruptions like the Ukraine war, dollar strength, and food and fuel supply constraints triggered inflation across Africa, national responses have determined its severity and persistence. Countries like South Africa and Kenya show that timely, well-communicated policies can cushion citizens. In contrast, delayed or abrupt reforms, as seen in Nigeria and Egypt, have intensified household burdens.

Nigeria offers a cautionary tale of reform without adequate social cushioning.

Macroeconomic reforms, such as fuel subsidy removal and FX liberalization, can be necessary for long-term stability. But in Nigeria’s case, the absence of pre-emptive social protection measures meant millions were left vulnerable to sudden price shocks. The result is a wave of hardship affecting transport, food access, and livelihoods, especially among low-income and informal workers.

Fintech and informal networks are filling critical financial gaps, but not without risks.

Digital lending, rotating savings groups, and AI-based credit tools are helping consumers stay afloat. However, these solutions often lack regulatory oversight, transparency, and long-term sustainability. Rising default rates and consumer over-indebtedness signal a need for stronger financial education and safeguards.

Regional differences highlight the need for localized, context-aware responses.

Inflation is not unfolding uniformly across the continent. Structural factors like agricultural capacity, import dependence, monetary independence, and political stability all play a role. Policymakers, lenders, and development actors must tailor their interventions to specific country realities rather than applying blanket solutions.

Lived experiences reveal the human cost of inflation in ways data alone cannot.

The voices of everyday Nigerians, skipping meals, trekking to work, borrowing just to buy food, or juggling side hustles to keep families afloat, bring this crisis into sharp, personal focus. From Lagos to Kaduna, respondents describe inflation not in percentages, but in sacrifices: “We’ve had to cut costs for things we normally get,” says a mother in Oyo; “I sometimes use loan apps just to eat,” shares a young man in Lagos. These real-world reflections illuminate the daily trade-offs hidden behind economic indicators, grounding this report in the realities that policymakers, funders, and innovators must urgently address.

2026 Enterfive Inc. All Rights Reserved